- Published on

Stablecoin Adventures in Crypto and TradFi

- Authors

- Name

- Abi Raja

- Follow me on Twitter @_abi_

The recent UST collapse prompted me to read a paper that's been on my reading list for a few months. Stablecoins: Growth Potential and Impact on Banking was published by the US Federal Reserve earlier this year. It's a good read with a substantial focus on how increased usage of stablecoins would impact the banking system. I'm not particularly interested in the effects on banks but obviously, the Fed is.

But the paper also gives a good, short overview of the basics of how stablecoins work and it's worth reading for that. It doesn't talk much about de-pegs, especially when the value of the stablecoin dips below the $1 peg as UST did.

But they do briefly discuss the scenario when stablecoins trade above the $1 peg such as during crypto market downturns.

If Bitcoin price is crashing quickly, people want to exit quickly by trading Bitcoin for a stablecoin. The increased demand for the stablecoin which the issuer can't keep up with will temporarily push prices above $1 since some traders are willing to take the small loss in order to exit their volatile Bitcoin positions.

Reading the paper also lead me down the rabbithole on a different fascinating topic: "non-crypto stablecoins".

Bank of England and George Soros

"Non-crypto stablecoins" are an old concept. Central banks sometimes like to peg the value of their currency to another currency i.e. a fixed exchange rate as opposed to a floating exchange rate determined by the market. The central bank has to spend money to defend this peg but it might be worth it for a government towards other policy goals such as keeping exports cheaper and competitive.

The most famous disaster associated with the depegging of such a currency is Black Wednesday. The Bank of England had agreed to a peg that overvalued the pound relative to the German mark. As an example, say you could get 1 pound for 10 marks. But since England had significant inflation during that time, the market was willing to take even just 5 marks for 1 pound.

Under such circumstances, you could short the pound like so:

- I borrow 1 pound from you (1 pound on hand, owe 1 pound)

- I sell it for 10 marks (10 marks on hand, owe 1 pound)

- I buy back 2 pounds with my 10 marks on the black market (2 pounds on hand, owe 1 pound)

- I give you back 1 pound and pay you a borrowing fee of 0.1 pound (0.9 pounds on hand, nothing owed)

That's exactly what Soros did, except he didn't buy the shorted pounds back from the black market.

When a central bank establishes a peg, it maintain some foreign exchange reserves. In this case, the Bank of England held billions of marks. So if you want to sell your pound for marks, they would give you 10 marks even if others were only willing to give you 5 marks. Of course, their foreign exchange reserves are finite, and especially so if they're having a hard time getting anyone to sell them marks for pounds. If people think 1 pound is only worth 5 marks, then BOE will have to buy marks at that price and take a loss of 5 marks (10 marks - 5 marks) every-time someone wants to sell a pound at the pegged exchange rate.

When Soros launched his attack by selling his borrowed pounds, the BOE started accumulating greater and greater losses trying to maintain a pegged exchange rate that was so much higher than the market rate. Eventually, they depleted their reserves, gave up and decided to let the exchange rate float. And now, Soros could buy back all the borrowed pounds he sold at a much lower price and pocket a handsome profit.

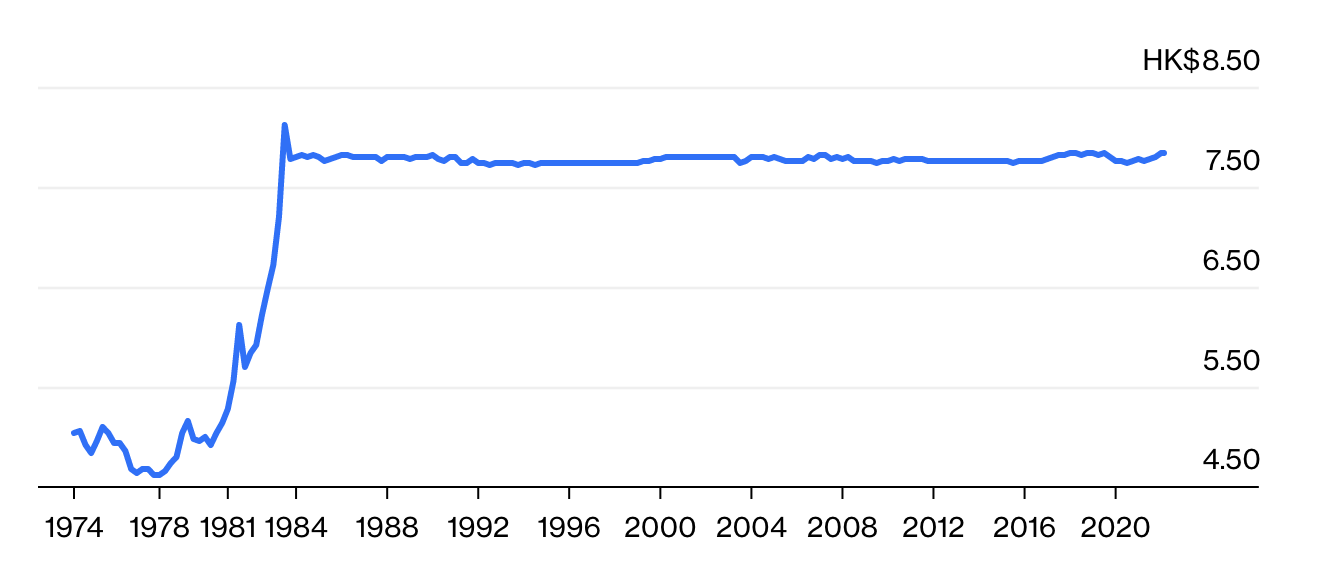

Hong Kong Dollar

On the flip-side, this piece in Bloomberg describes how a different currency has successfully defended its peg for almost 40 years: the Hong Kong dollar:

The Hong Kong Monetary Authority runs a pure currency board. All of HKMA’s monetary base is backed 110% by US dollar assets. Second, while fixing the exchange rate, the authority deliberately lets interest rates float freely to absorb pressures on the peg. When the local currency gets sold off, there’s a capital flight from Hong Kong. But that automatically raises interest rates enough to lure buyers back.

Of course, a higher interest rate means your economy has to be doing well enough to afford it. In Hong Kong's case, this has been true for the last 40 years and they've managed to successfully hold this peg at HK$7.50 to 1 USD.